The recent Dow sell off had sent shockwaves around the world. The sell off has triggered the 10% stop loss for Emperor Capital. Also, the sell off created many major opportunities for us to pick up undervalued stocks, mainly, Capitaland & Yanlord Land.

Capitaland have been on our watchlist for a long long time. It’s a strong blue chip stock in the property development industry which we believe will benefit from the recovery in property prices this year. Furthermore, Capitaland is grossly undervalued for a blue chip company. With a PE of 9.75 and NAV of $4.38, it gives us a huge margin of safety at our entry price of $3.60.

As we can see from Capitaland’s chart, it has hit a high of $3.87 in January 2018 in speculation that the property sector in Singapore will rebound. The trend is similar across many developers like City Developments, UOL and many more. The Dow panic caused it to drop all the way down from the peak to the support level at $3.45. Recovery in prices and frequent share buybacks by the Capitaland’s management up to $3.67 per share prompted us to enter this stock with it’s juicy margin of safety and potential rerating of the stock.

As for Yanlord Land, it was a case of insider buying and the perfect Dow crash that prompted us to look at it. Yanlord Land is also a property developer listed in the SGX, however most of their businesses are in mainland China. As it is an S-Chip, we were especially careful when researching and limited our risk by allocating a smaller portion to it.

The CEO bought back the shares aggressively from $1.58 all the way to $1.886 spending more than $5 million on Yanlord shares. That prompted us to dig deeper into the company. We realised that their 9M2017 results were actually fantastic and we were speculating that the FY result will be even better considering the CEO major buying of the shares.

Also with a PE of 5.7 and a NAV of $2.252, it presents us a juicy margin of safety as well. Knowing that the CEO bought so many shares, we entered Yanlord at $1.60. True enough, the FY results was good and they declared a higher dividend for the year. What we are speculating for Yanlord is that the CEO could be trying to privatise the company given the good business and how undervalued his company is right now. Only time will tell if this is true.

In conclusion,

having a watchlist of stocks and to capitalise on the stock market panic have gave us a favourable entry into these 2 stocks. As the saying goes, buy when others are fearful and sell when others are greedy. In actual fact it is never easy to do so. It was actually the clear margin of safety that gave us the conviction to enter the market when it is still suffering from the sell off.

We are one week into 2018 and most of us would have set our New Year’s resolutions for the new year! And it’s important to do that for investment as well, so that we know what are some of the rules guiding us in the year ahead.

2017 have been a rather uncertain year, and it’s also my very first full investing year (since I started in March 2016). I would have to say that I truly learnt a lot from my friends over at IN and from reflecting upon all my investing decisions throughout 2017.

A Quick Reflection of 2017

2017 was an exciting yet frustrating investing year for me as I started 1st Quarter of the year by hitting a multibagger. And then things went rather slowly for me as the next few stocks that I picked took rather long before showing any forms of gains. Most of them were range bound, and prices hover around my purchase price.

Some lessons I learnt in 2017 includes:

1) Buy towards the end of the week to avoid being trapped by traders.

2) No matter how good a stock is, it is vulnerable to the macroeconomic conditions. There were several times where the global markets was on a downtrend due to macroeconomic instability (like North Korea shooting missiles into the water etc). Those times were the true tests of emotional discipline to stick to your investment plan as all the stocks that I am holding can start recording losses as big as 5 – 10% in a few days to weeks.

3) Always buy stocks with the abilities to catch the industry’s tailwind. In 2017, semiconductor stocks were very much in play and many stocks in this industry recorded at least 50% increase in share price. I guess what many investors’ meaning of “a rising tide lifts all boats” was pretty clear last year. Some semiconductor companies who have weaker fundamentals did not rise as much but still were able to clock in a decent share price appreciation due to positive industry sentiments.

Those were the 3 big lessons I take away from 2017 and sadly to say my own portfolio didn’t outperform that of the STI but I will definitely give it another shot this year!

Now looking on to 2018!!

Looking ahead!

I am looking forward to an even more exciting year ahead as I am rather big on three themes in 2018. Mainly the O&G, construction and property industry. By applying Lesson 3 that I learnt in 2017, I will be parking more funds to catch the positive industry sentiments by investing in good qualities stocks in those industries.

I shall share a little more on why I feel these 3 industries should outperformed the rest in 2018. For O&G, the industry was hardest hit in late 2015 as oil prices started crashing until it hit about US$20-30 per barrel which is too low for many O&G companies to make a decent profit. These caused the industry to consolidate as many smaller companies went bankrupt or were bought out (like Ezra, Ezion etc) This was because many companies took on huge loans to run the company when the prices of oil were very high and when the oil prices crash they weren’t able to finance their debt as their main source of revenue is heavily affected. Now in 2018, oil prices have gradually been recovering and are now sitting near US$60 per barrel. As with all economic cycles, the period after consolidation is the time most O&G companies that were stronger will tend to survive and ride the next uptrend. (Survival of the fittest haha)

Thus I am looking at strong O&G companies with low debts to ride on the potential uptick in the O&G sector.

As for construction and property, its more for local play. Construction sector have been the weakest link in Singapore GDP as it continues to post negative growth in 2017. The construction sector is a labour intensive industry that have not been disrupted by technology. The government have been encouraging the use of technology in the sector to raise productivity in order to lower costs. However, it has not been working as the initial costs of taking up new technology is high and having more competition from foreign construction firms has led many local construction firms to not make the switch. However, the government intends to support the industry by bringing forward more construction activities. With major developments, like the T5 and MRT lines yet to be build this should inject some activity into the constructions sector this year.

Also, there have been a spate of enbloc activities carried out by property developers in Singapore. This should help to boost the construction activities in Singapore too as the acquired buildings will have to be demolished and rebuild.

With private home prices rebounding slightly in 2017, developers are rushing in to stock up their land banks in hope to be able to build new properties to catch the uptrend in private property prices. This represents an opportune time to invest in construction related stocks with support from both the public and private sector this year. Property developers that have many new private property launches this year may benefit from stronger demand due to a possible rebound in private property prices to cash in on their developments.

In conclusion,

these are the areas where I should be parking most of my funds in hoping that a rising tide can lift all boats. My search for undervalued companies in these industries continues and hopefully I will be able to catch some of them before they fly! 🙂

Hi everyone, this is my first post since I got back from being deployed overseas for a month in Australia. Happy to finally be able to have some time on hand to do things I like. Recently, I read this article on Medium called “Confessions of a 23-Year-old thousandaire”. In the article, he wrote about his financial journey as a 20 odd years old individual in the US. I was inspired by it and thought I should do a Singaporean edition based off my own experiences. I hope teenagers or even those in their 20s will glean something off my CONFESSIONS. Haha so here goes…

Chapter 1: Who says you got no money?

There is always this common misconception that teenagers like us have no money. True enough we don’t draw a constant salary unlike our parents. But we do draw a steady stream of pocket money from them. One thing I regretted when I was drawing pocket money from my parents was to draw it daily instead of weekly or monthly.

Drawing your money weekly or monthly is a better arrangement as it forces you to learn BUDGETING. You will need to learn how to allocate your money wisely throughout the week or month in order to have sufficient for each day.

Budgeting is a critical first step in learning how to plan your money wisely. It was only until NS when I stop taking pocket money from my parents and start living off my own NS salary that I realise the importance of budgeting. On some days, you can very well spend a few times more than you are supposed to, so remember to always BUDGET!

Like they say:

“Failing to plan is planning to fail.”

Chapter 2: Save yourself by saving…

To tell you honestly, I didn’t even realise the importance of saving until I was 18. I regret not saving up left overs of my pocket money into my savings account. Usually my leftover cash will stay in my wallet and mysteriously “disappear”. Haha it probably went into my stomach with all the snacks or occasional Starbucks that I bought.

The lesson here is by not saving and leaving cash in the wallet, it exposes us to several dangers lurking out there. By dangers I mean temptations to buy things that you probably won’t need.

With the advent of cashless payment, it becomes even more important to be discipline in your budgeting and saving habits. You will not feel the pain when you just click a few buttons to purchase whatever things you see online. The pain only comes when you check your bank account at the end of the month.

Don’t belittle the small amount you save each day, be it from your pocket money or your monthly salary. It is these small amounts that will pave your way to financial freedom.

“The habit of saving is itself an education; it fosters every virtue, teaches self denial, cultivates the sense of order, trains to forethought, and so broaden the mind.” — T.T Munger

Chapter 3: Make your money work for you…

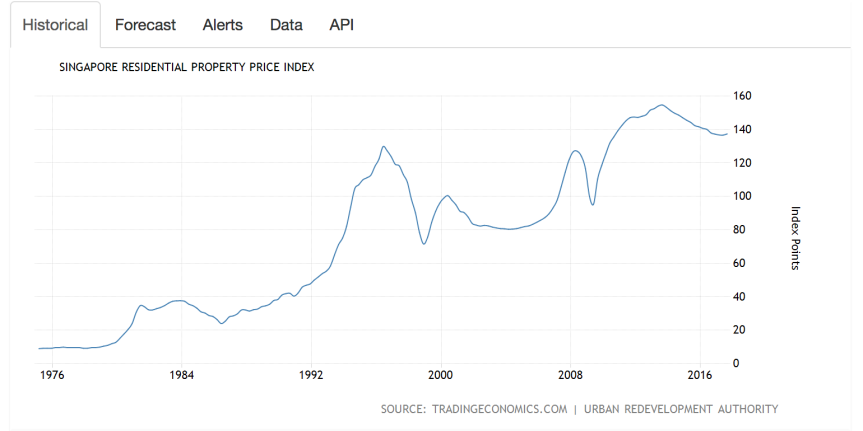

Sadly, in our times, it is no longer enough to just save for retirement. Inflation is continuously eroding the value of our savings 10, 20 years down the road. Inflation is the reason why our $2.50 chicken rice is now $3.50. Here’s a chart showing the price of property for the past few decades.

The one clear trend here is UP. Of course, wages have also been growing but the paramount question will be if wage growth can always outpace the rate of inflation. And even so, all those money you save up in the bank are only going to depreciate in value as inflation rate outstrips the interest rate gained on your savings.

Hence, we need to have some ways to make our money work for us. And that is through investing. Whenever I tell others about investing, many tend to look at me with fearful eyes. Even my mum advised me against investing, because to her its akin to gambling. What many don’t know is that investing can be a safe and fuss free way to grow your money.

Average inflation rate is about 2-4% per annum. Banks currently give you about 0.05% on normal savings account. To win the game of investing, all you need to do is to ensure your money grow at a higher rate than inflation. Sounds tough? It’s actually quite easy.

For those who don’t intend to actively manage their investments which usually yield higher returns albeit at a higher risks, index ETFs are safe and fuss free way to win the game of investing.

The above are 2 of the indices that track a group of stocks. S&P 500 tracks the best 500 US stocks and FTSE tracks the best UK stocks. As you can see as long as you are able to hold it for a long time, the trend is only UP. S&P 500 annualised return since its inception is about 10% per annum which is much higher than the inflation rate. The FTSE return about 5% per annum for the past 20 years also higher than inflation rate. Hence putting your money in the best stocks in the world through index ETFs are definitely an easy way to make your money work for you.

There are also many other methods to invest for beginners which I shared in this article

“An investment in knowledge pays the most interest.” — Benjamin Franklin

Chapter 4: Compounding is the key to financial freedom…

The key to a fruitful retirement in the future is through compounding. Imagine someone were to give you 10% every year on the $1000 you put with them.

You will realise that you do not just get $100 every year. The amount earned increases exponentially with time!

Now imagine 2 individuals, Adam and Smith. Adam starts investing with his $5000 savings at the age of 20 by buying into the index ETF that return 10% per annum. On the other hand Smith started slightly later at 30 buying into the same investment product as Adam.

Assuming they both aim to retire by 65, how much retirement sum would they have?

For Adam:

Wow a sum of $364,452.

As for Smith:

The difference is HUGEEEE. A 10 year difference means your results are reduced to about HALFFFF!!

So who says you can’t start investing with a few thousand dollars? The magic of compounding usually sets in the longer you hold onto your position.

The lesson here is start picking up investing EARLY and have PATIENCE to let your money do the work for you.

“Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.” — Albert Einstein

Chapter 5: Enjoy the process…

The most important thing of it all is to enjoy the process. There’s no point to save up such a huge amount of money but lead a miserable life of cooping yourself at home in order to save up a few penny. At the end of the day, you can’t lug your bag of cash with you to the grave. I ever once tried to save 90% of my NS salary and only spend 10% of it. It was tough and I found that I wasn’t happy. That is not to say that you abandon saving altogether, but rather plan your budget around your lifestyle and find a healthy amount to save and invest. This is so that you can both enjoy the PRESENT and the FUTURE!

“Enjoy the process. You will get there, you might as well enjoy the journey!”

In conclusion,

the whole idea of me setting up this blog is to educate young people to take charge of their financial journey early. You don’t need a lot to start From Ground Zero, I started out with $300 in the stock market. You just need to be patient and disciplined in budgeting, saving, investing and the rest will take care of itself. Hopefully this will encourage more young people to take charge of their finances! 🙂

Hi all!! It’s been a while since I did a [Building Blocks] post. Haha if you were an avid reader of my blog, you will realise that I have been posting quite a bit in [Eye Candy], the segment where I do some analysis on stocks I am researching. Yup I have been rather busy digging through the stock market for gems that I could put my money into. As you can see from the title of the blog post, today I will be trying to help you understand your FIRST step to financial freedom. This FIRST step is essential as it lays a foundation for you to work your money. In other words, in order to INVEST your money you need to embark on this FIRST step.

So what is this FIRST step that is soooo important??

The answer is: SAVING!!

All of you might go “Duh” but how many of us are actually able to really save up your salary or money? We often have the goal to save up this amount but most of the time we give in to certain pleasures and decide to spend almost all our salary away. I know this because I myself is guilty as charged haha!

When I entered the army, its the first time whereby I was drawing a constant stream of income (unlike those adhoc jobs I did last time). With sudden inflow of money every month, I did not have a concrete saving plan and hence my expenses were very high at the start. In some months, I may be broke without the month coming to an end. I also know of friends who are like that too! I only started taking charge of my savings when I started investing as I realise how meagre my savings are.

So I started reading up and created a system to force me to save, but before that let’s look at

1) The importance of saving

Saving is an important first step to your financial freedom because without savings, you will not be able to use that money to work for you. Imagine yourself spending every dime of your monthly salary, how will you be able to put any money into investing in stocks, property and so on. So if we ourselves do not understand the importance of saving it’s hard for us to grasp the power of investing and compounding!

2) Saving can be automatic!

Yes it can be. Nowadays with the advent of technology, most of us definitely have an ibanking account with any of the banks in Singapore. And it’s super easy to automate the entire process of saving. Let me show you how.

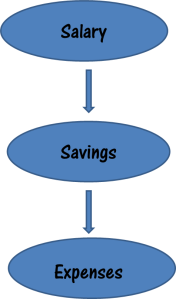

First, you will first need to set up 2 bank accounts

Yes, create 2 separate bank accounts, one for purely savings, the other for expenses only.

Secondly, credit your salary into your savings account. After doing that, calculate a rough percentage of your monthly expenses. For me, I save about 75% of my salary and spend the other 25%.

Finally, set up an automatic transfer between the two accounts. Transfer the percentage for your expenses from your savings account to your expenses account.

Yes the end result should look something like the flow chart above.

3) Don’t touch your nest egg for fun!

Yes! You read it right! Don’t touch your nest egg (savings) for fun (entertainment). Put it another way, don’t spend your savings!! For me, I practise that by not bringing out the ATM card that belongs to my savings account. That way I will not be tempted to dip my hands into my savings.

Of course with that said, what if its an emergency and you need the money? If it’s an emergency, then I guess there will be no choice but to tap on your savings. However, if possible try to reduce your expenses in the subsequent months to repay the amount you took from your savings.

One point to note is that you should always ensure you plan a right amount to be set for your expenses. I tried to save 90% of my salary before, but it’s just too tight on me and I tend to keep tapping onto my savings because I ran out of money. So plan the amount carefully so that it does not give you ANY temptations to tap into your savings!!

In conclusion,

you might say that as a young person, saving is very insignificant to you since you probably can only save a few hundred a month. But take that few hundred and multiply it by 12 or 24 months you are looking at a few thousands already. Think BIG! And that’s not all, use your nest egg to work for you through INVESTING! Slowly but surely, this small amount will grow and compound.

I really like the picture above. In the very first picture I showed you a hand dropping coins into a jar which signifies saving. And with your savings, it forms the soil and fertiliser to grow your money just like the above picture. Savings is a cliche topic and whatever I shared above may be shared by many others too. But, what I think is most important to you is TAKING ACTION to really start your saving plan because saving is the FIRST step to your financial freedom!

** Haha side note before I end. I have been toying with the idea of helping people who are keen to get into investing. I am still working out how should I deliver it. So do stay tuned for more update on this! 🙂 **

Hi all, apologies for not posting for a while now. Peak period of outfields week in week out made me procrastinate for quite a bit haha. I realised it’s been about 1 year since I started investing. A lot had happen and I am thankful for the many lessons I have learnt over the course of the year. All that happened, made me stronger and allow me to continuously revise my own investing strategy. Today, I shall share about my own investing strategy. How I identify potential investment targets, what I use to time my entry into a stock and when to sell.

1) Investment Objectives

Previously, I shared the importance to know your own investment objectives before being able to craft out your own investment plan.

Your own investment strategies are the actions you are going to take in your investment plan. Just a recap, for now my investment objective remains to grow my capital. From a measly sum of $300 at the very start of my investment journey, I am targeting to grow it to at least $10k before I enter the university. (Of course along the way, I added more money into my investment.) As of now I have about $6k vested in the stock market and sitting on a 20% realised return so far. Below is my investment strategy I am using to reach my objectives.

2) How I pick my investment targets

Personally, I like to look for companies with low Price to Earnings (PE) ratio with huge growth catalysts ahead. Companies that are of such qualities fill up about 60% of my portfolio. The reason why I adore such a company is because it is both undervalued and have ample of growth characteristics. (Killing 2 birds with 1 stone!)

Of course, sometimes it’s hard to find such a company. But all you need is that 1 or 2 opportunities to give you astronomical gains. Examples are companies like AEM which was previously PE of 8-9 (undervalued) and had a innovative product (growth). When the market comes to realise the company’s potential, the share price will readjust upwards.

After finding that few value-growth companies, I like to diversify across themes. By that, I like to research their growth areas and see if it fits any major trends happening in the world or in Singapore. For instance, now the One Belt One Road is quite a big thing, companies (construction, railway builder etc) that are undervalued and have operations in this area will potentially stand to gain from the growth opportunities available. Here’s another example, I may want to look at a more defensive theme. Companies that are undervalued and are in the industry that provides services to consumers, governments etc are all plausible candidates.

Of course, after shortlisting the few that make the cut. Checking their fundamentals is next and even better if there has been insider buying. (Here’s how I evaluate a fundamentally sound company)

3) Timing my entry

After all that filtering process, you should probably be left with a list of less than 4 companies. Timing my entry to buy into the stock is next. How should I buy at the correct timing. For me, some technical indicators and the chart have helped me quite a bit.

I like to enter my first position after a period of consolidation (where the price have been around the same level for a few weeks) and with low volume.

I use the weekly chart for a better long term view since I usually hold my position for a few months at least. The red rectangle is the period of consolidation where prices close in very tight range. And if you look at the blue circle, the volume is below average for those few weeks. This represents a rather good opportunity to enter. I like to see consolidation period as a spring board to propel you upwards. But, how do we tell if price will go up after consolidation and not down?

I use the MACD indicator to see if there’s a possible uptrend coming. (I am not going to go too in depth into indicators) When the blue line cross the red line as shown in the circles, it is a possible indication of an uptrend. For me, I only use indicators as an additional reference after I spot a consolidation zone.

4) When to sell?

Haha to be honest, this question always baffles me. I myself am also not a good seller. There are a few times a stock raced upwards after I sold away all my position. Sometimes, I get to emotionally attached to a stock and tend to sell too late. Hence, this portion is something I am constantly still learning. However I do have a few ground rules to follow.

Sell when the undervalued stocks become overvalued.

Sell at your stop loss.

Sell when the business is no longer attractive or fundamentally sound.

I don’t really use technical indicators to predict when to sell, because I believe that as long as the business’s value and growth aspects remain intact, a downtrend should be temporary.

In conclusion,

planning your own investment strategies to achieve your own objectives is important. You need to know what stocks you are looking into, when to enter and when to sell. Only then will it translate into gains in your portfolio. Hopefully for those who started investing, you will be empowered to write out your own investment strategies after reading my own strategies. Writing it out is really effective, as it makes sure you do not get flustered when anything happens in the market.

Hi everyone, it’s been about 3 weeks since I last posted. Was away for a military exercise in Thailand. A lot have happened while I was in Thailand, the weather was crazily hot, GID outbreak in camp and I also sold one of my stock holding that gave me a 100 percent return on investment. The profits made from that investment was able to cover out all my losses incurred when I just started out investing. Today, I will be sharing more about the characteristics of that stock and the things I have learnt from this episode.

1) 100% return in just 3 months?!

Yup I was equally surprised! Some of you may have noticed that in most of my recent posts, I have been using AEM Holdings as an example. Yup this is the company that have became my very first multibagger (a stock that returns more than 100%). It all started out when I was screening for low PE stocks in the SGX. (Value approach). This company popped out in the screener which caught my eye. It has innovated a cutting edge product that no one in the world has been able to and back then its PE was less than 10 (relatively undervalued). The company have also just returned to making profits and are planning to ramp up the production of this product which means that further earnings growth is guaranteed.

Since it fulfills the basic principles I set out for a fundamentally sound company and I read an interesting piece of analysis by the guys over at thelittlesnowball.com which reaffirmed my beliefs, I vested into the company at $0.885 per share.

From the chart, I entered AEM at $0.885 per share, added more shares at $1.055, before selling them at $2. If you were wondering why did I decide to sell it instead of holding onto it longer, it was because this stock was about 60% of my portfolio. I have about $2000 invested in it. As this stock catches the attention of more people, it will become more volatile as big players come into the fray. Since I am just a small fish in this, I decided to take the money off the table and only enter again when there is a dip in prices.

Not all company can be like AEM, which gives a 100% return in just 3 months but there are certain characteristics that the company possessed.

Growing earnings

No debt

Frequent share buybacks

Undervalued

and most importantly it has major catalysts (in the form of their cutting edge products) coming its way.

2) Lesson learnt from this episode

I think the most important lesson I learnt from this episode is to be consistent in your approach. A lot of times, young investors like us tend to be swayed by our emotions. For instance, chasing the next hot stock etc etc. When we are swayed by our emotions, we tend to forget all the framework that we set in place for ourselves. Hence being consistent in our approach and calm minded are very important when we are investing.

This episode also shows that you do not need to be in many trades to profit from investing. Sometimes, all you need is that 1 stock to do the magic. Hence, when you are disappointed because you had to be force to exit a stock due to the stop loss in placed, remember that 1 win can easily make up for many small losses if you exit them early. Personally, I was down about $600 since I started investing and this was still when I didn’t learn to cut loss. In that $600 includes the 70% lost incurred from my Noble’s debacle. I am glad that my revised approach, have led me to recover from my losses and rake in a small profit.

In conclusion,

I would like to say that not all stocks can be like AEM. However, many stocks do have some resemblance to it. With enough due diligence, and a small leap of faith you may just stumble upon the next AEM. Most importantly, do not forget the framework you built for yourself while investing. Personally that has been the most important rule that led me to find this undervalued gem!

Hello everyone! Hoped that all of you had a great CNY holiday. Haha since I am now on my CNY block leave I decided to write today. In my previous few “Building Blocks” blog posts, I have talked quite a bit about the different styles of investing and the all so important investment objectives that everyone should have before investing. Since we are all richer due to our red packets (for those singles out that :P), I thought it is timely that I should touch a bit about how to actually get started.

Off my head, I thought of a few questions that a new investor would have when he/she is starting out.

How much should I invest?

What to invest?

How do I go about doing it?

(Do reach out to me in the comment box if you have any more questions about investing. :). I will do a separate blogpost to address those questions if any haha)

There are 2 investing instruments that I would recommend a young and new investor to consider that would answer the above questions.

1) Regular Saving Plans (RSP)

What to invest?

RSP is a great way to get started on investing. Most of the banks in Singapore offer RSP, but since most people are account holders of DBS or OCBC. I will mainly touch on the RSP programme that the 2 big banks offer. For me, I would recommend against investing in mutual funds because they tend to do worse than the general market in the long term. I would prefer a RSP in an index fund or an Exchange Traded Fund (ETF). Both the index fund and ETF are created to match the performance of the broad market. For instance, the STI ETF is created in a way to match the movement of the STI (the top 30 companies in the SGX). So whatever happens in the market, will be reflected in the fund. Also, sales charges for these type of funds are generally cheaper than a mutual fund because there are lesser transactions (less actively managed) made by the fund manager.

So how does a RSP works? A RSP invest a fixed amount of money every month into the fund you are intending to invest in. For instance, you could do a $100/mth RSP in the STI ETF.

RSP is mainly for those who want to invest for the long term and may not have a huge upfront capital to invest at one go. Think of this like putting your money into a piggy bank that yield higher interest rates than your normal banks’ interest rate.

If you hold this STI ETF for 5 years you will get a pretty decent 4.66% return compared to the bank’s non-existent interest rate

How much to invest?

This question will really depend on yourself. How much will you be able to take out from your monthly income to ensure that your living expenses etc are not affected. Since the RSP will only see fruition in the long term, cancelling the plan midway is not very beneficial to you. Hence, it is really up to you to decide the amount. In SG, the minimum amount to put in an RSP is $100/mth.

How do I go about doing it?

DBS and OCBC both have different types of RSP. You can only get an RSP with them if you are an account holder of the bank. For both banks they offer investing in RSP in unit trust. Do note that unit trusts are usually investment in mutual funds which I do not really recommend. (But of course if the funds have a good track record of returns then by all means). What I would recommend is their RSP in ETF and equities.

For DBS, their RSP allow you to choose between the NIKKO AM SG STI ETF (the one shown above) and ABF SG BOND INDEX FUND (which invest in the bonds of SG)

For OCBC, their RSP is different from DBS, OCBC allows you to invest in blue chip companies in the SGX. The plan is called Blue Chip Investment Plan. Basically, the same concept of RSP applies but they invest your money into a blue chip counter you choose monthly. Of course the charges are a bit different for this plan.

For more info on OCBC Blue Chip Investment Plan, click here

Summary

The RSP is a very powerful tool and forms a relatively risk free investment vehicle for starters, but it must be held for the long term in order to realise the gains. For young investors who may not have a monthly pay now, this could be a bit of a problem as you may need to scramble enough cash in your bank account before the investment date every month. Ultimately, you need to carefully plan your expenses before you embark on this plan.

2) Investing directly in the stock market

What to invest?

The other way to invest is to invest directly through the stock market. Imagine the stock market as a big supermart and in the supermart there are a myriad of products on the shelves. Some may be more expensive but of better quality, some may be cheaper but of poor quality, some may be a new product that has just arrived etc etc. The trick here is to pick the right product that suit your personal taste and preference. And all this can be answered by your investment objectives. The stock market can be categories into 3 groups in terms of risk level.

If you are new to the market, you can consider your first stock to be something relatively of lower risk like an index ETF or a blue chip (Do note that there are many other ETFs too which have different objectives.) Slowly, as you learn more about how to evaluate a company fundamentally and technically based on their chart (which I will also share with you in future posts) you can invest in normal equities while minimizing your risk.

How much to invest?

This is again a subjective question. But I will share with you some pointers I learn while investing in the stock market with little upfront capital. Firstly, the commission for most brokerage houses in SG is at least 40 SGD for a two way trade (Buy and Sell). So the lesser the amount of money you invest in a stock, the larger the percentage that the commission will stand in your profit. Ultimately, you want to make a profitable trade so taking into account the commission is very important. Secondly, with lesser amount of money, the multiplier effect of your stock is much lesser. For instance, someone with 1000 shares will make more money than someone with 100 shares given the same percentage increase.

All in all, the commission cost is the first hurdle to cross before you can be profitable in any trade. And using the multiplier effect will greatly increase your chance of beating that first hurdle. So how much to invest depends on whether you can understand the risk reward ratio of the stock you are planning to invest and giving it sufficient amount of money to beat the first hurdle. For me, I always try to purchase at least 1000 shares in the stock that I plan to invest as it set a nice $100 return for every $0.10 increase in stock price.

How do I go about doing it?

First and foremost, in order to start investing in the stock market, you need to have a brokerage account that is connected to the Central Depository (CDP) which stores all the shares you buy in the SGX. There are several brokerage houses in Singapore, I will list out a few.

DBS Vickers

OCBC Securities

Philip Securities

CIMB Securities

Majority of the brokerage houses in SG charge about the same commission fees. A minimum of $25. Some brokerage houses have special programme to differentiate themselves. For instance, DBS Vickers Cash Upfront Account only charge a commission of $18 for buying. For brokerage houses that are owned by banks like DBS and OCBC, they would usually require you to have a savings account with them. 3rd party brokerage houses like Philip Securities doesn’t require you to do so. For me, I chose DBS Vickers because I am already using their savings account which save me the hassle to open another savings account with another bank. You do have to be at least 18 in order to open a brokerage account with some of the brokerage houses. Some require you to be at least 21. Hence it is important to research each brokerage houses first before signing up with them and you can have several brokerage accounts with different houses.

Here’s a good article to help you in choosing a brokerage house.

In conclusion,

these are the 2 ways I put forth for new investors to go into investing. Do always remember to do your due diligence before plunging into any decision and allocate your money well. That’s all from me today. If you have any questions, I would really love to hear them. Simply comment below and I will do utmost best to answer each one of them. Adios! 🙂

Hello! Hoped everyone had a great New Year Day holiday. As mentioned in my previous post, today I will be sharing with you about my own investment objectives and my reasons for it.

I have done up a simple diagram of my own investment objectives. I prefer splitting my investment objectives in period of 5 years so I can have a holistic view on how my investment style changes with the years.

In 5 Years:

Why: As some of you may know, I did not start out with a huge upfront capital in investing. The average size of my trade is only a few hundred dollars per transaction. The multiplier effect of investment increases when more shares are bought. Hence, I decided to dedicate my first 5 years of investing to aggressively growing my capital. Since, I am in the army and will be in the university during this period, my tolerance for risk is much higher.

How: I will do so by looking into growth and value stocks which have higher potential for price per share appreciation. I will try to lock in at least 20% gain in price before selling the shares completely. Hence my holding period is not very long term. With that, it is also important to protect my down side. When I started investing, I did not actively pursue a stop loss and caused a great deal of problems for me. With such high risk pursuit of capital growth, having strict stop loss is important to protect your downside risk.

Characteristics:

Look for growth and value stocks

Sell when stocks appreciated at least 20% in price

Strict stop loss to prevent down side risk

In 10 Years:

Why: After the 5th Year mark, I should be out in the working world and making a regular income. Although I would still be young, its important to start saving for retirement. Hence, the percentage of my portfolio changes with an extra element of preserving my capital. Overall, I am still growing my capital but less aggressively compared to 5 years ago.

How: Likewise, I will continue to look for growth and value stocks to fulfill my investment objective. The added component would be to source for income producing assets, like blue chips, bonds, fixed deposit to preserve my capital.

Characteristics:

Look for growth, value and income stocks

For growth and value, same rule of selling when price appreciate at least 20%

Same strict stop loss for growth and value stocks

For income stocks, look for blue chips that pay regular dividends. Preferably reinvest those dividends.

In 15 Years:

Why: After the 10th year mark, I would be in my 30s with much more responsibilities. Most of us would also get a HDB in our 30s. This will incur more expenses and hence it is more wise to be less risky and protect more of your capital. Hence, preserving capital becomes more than half of my portfolio.

How: Pursuit for growth and value stocks become less important. Looking for stable income producing asset becomes paramount.

Characteristics:

Look for more income producing assets

Same rules applies for growth and value stocks

In conclusion,

its important to know how your investment journey will span out. Having a investment plan with clear investment objectives should help you make accurate investment decisions. When I first started out, I did not have such a plan, I plunged myself into different trades like a headless chicken and incurred heavy losses. Do not make the same mistake I did haha. Of course, life is not smooth sailing like you want it to be. Things change and crisis may emerge, thus it’s important to always review your investment plan and objectives yearly and tweak them accordingly. For those who may have yet to have an investment plan, feel free to try out my method of planning and let me know if its helpful. Here’s to a great 2017 for all of us!

In my previous post, I talked about the styles of investing that majority of investors subscribe to. In it, I also mentioned that knowing one’s investment objective is key to understanding oneself before plunging into the investment world. To be more specific, by investment objectives I mean what do you hope to get out of your investments. Is it short term gains or long term income investment? Most of us should be working towards long term income gains. Thus, knowing what you want to achieve out of your investment will guide you along when you are making your investment decisions.

How to determine your investment objectives?

There are really no hard and fast rules to go about this. However, I would like to present some guiding questions which may help you go about crafting your own investment objectives. These investment objectives should be the main overarching lighthouse that guide your investment decisions.

1) What’s your risk appetite?

Are you someone who can sleep well at night if say your stock took a 10 percent plunge during the trading day? Or are you the type that worry even if the stock were to fall slightly. These questions are important because investing shouldn’t stress you out too much and compromises your health. You should look for something you are comfortable with and invest in it. Typically, a younger investor would be more risk adverse because they know that their investment time frame is longer than someone in their 50s or 60s.

2) What’s the proportion of your savings you are using for investment?

If you are putting up 90% of your savings to investment then it is important to diversify your portfolio with safer stocks because a large portion of your savings are inside it. I am not saying that its wrong to use 90% of your savings to invest. Just that if you are putting such a large proportion it pays to be a bit safer with it. By answering this question, it should help you decide how to distribute your money in different investments of different risks.

3) Are you short term or long term?

Are you someone who gets excited over small price increase and are eager to sell it to realise the gains or someone who is very patient and wouldn’t mind to wait for 10 years to realise the gains? This is important because it will determine what kind of stocks you will tend to choose. Those who are short term tend to trade on price action, are quick to take the profit off the table and then plunge into another trade. Someone who is short term takes on more risk than someone who goes for the long term since there have been more bull markets than bear markets in the long run.

By answering some of these guiding questions it should give you a better understanding about the type of investor you are and what is at stake. Only when you know the type of investor you are can you go on to set a relevant investment objective and subsequently your style of investing to achieve your objective.

For me personally, I plan my investment objectives in 5 , 10, and 15 years so I get a holistic view of how my investing objective and style will change eventually. For instance, in 5 years, I am looking for more short term gains to quickly multiply my capital before I switch more towards looking for dividend paying stocks for the long run. I will share more about my investment objectives in the next post. That’s all for today! Have a great Christmas ahead! 🙂

You will realise that you do not just get $100 every year. The amount earned increases exponentially with time!

You will realise that you do not just get $100 every year. The amount earned increases exponentially with time!