In the recent announcement by GSS, it have announced the long waited results of their oil and gas venture. I mentioned in my previous post on GSS that this catalyst is the most important for GSS in 2017 as it determines whether a not their O&G business arm will be successful. I also previously shared on IN that the most uncertain part of any O&G business is the exploration phase as a company can spend millions on setting up the place for drilling but if they can’t find substantial oil in the area, its a failed effort.

And yes! They did it. The management’s postulation on the Trembul area seems to be right.

And yes! They did it. The management’s postulation on the Trembul area seems to be right.

In this post, I shall made a new set of possible postulations of what might happen from now on for GSS after reading the various articles and reports about GSS after they have found oil.

Summary of Announcement

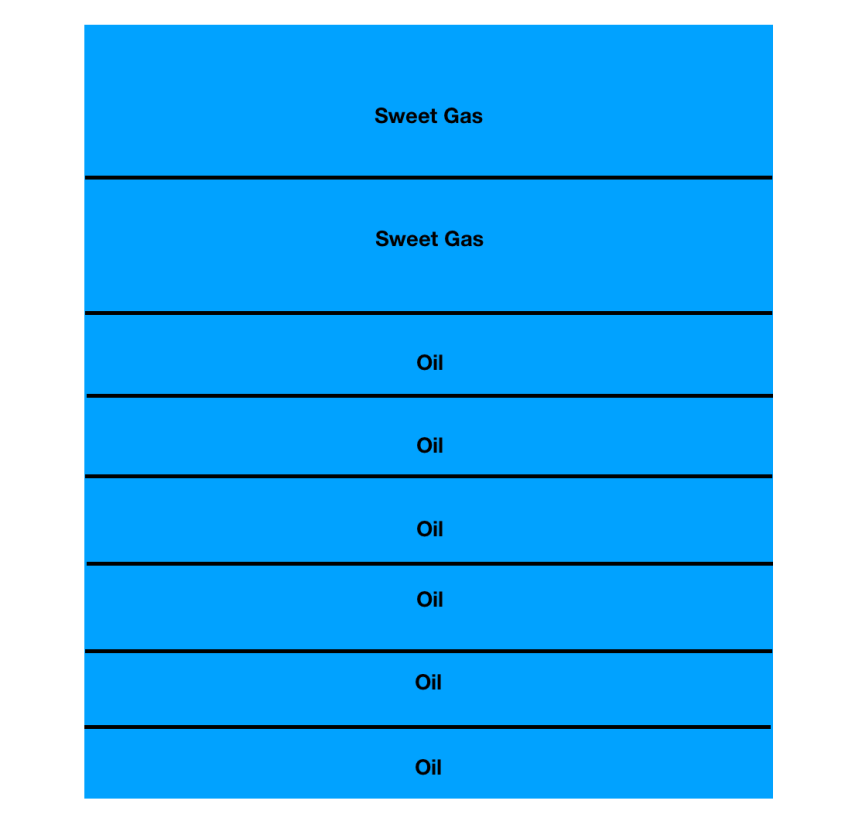

According to the announcement released, there are 8 columns of hydrocarbon found under SGT-01, the well that they drilled. The first 2 being gas and the next 6 is oil.

And according to in-house estimates, the 1P (proven) recoverable resources in SGT-01 is 2.83 million barrels of oil from the 6 oil zones and 8.49 BCF (billion cubic feet) of sweet gas (equivalent to 1.5 million standard cubic feet per day (MMSCFD) of sweet gas for the period of 14 years).

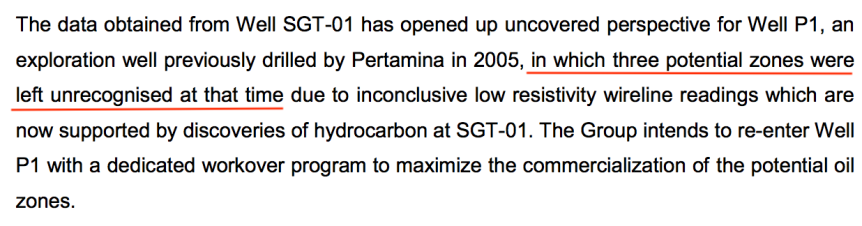

I believe that the management was very wise in choosing that location to conduct SGT-01 well exploration as it is near several other old abandoned wells which allow them to also be able to deduce the oil profile of those older wells. Because of this discovery, they were able to estimate more accurately, the oil profile in well P1 that was drilled by Pertamina back in 2005. (Well P1 have more than 3 potential oil pay zones).

Also, GSS have shelved asides plan to drill SGT-02 which was supposed to be done after SGT-01 to drill the surrounding wells near SGT-01 so that revenue can be recognised from this discovery. Another wise move.

GSS will look to monetise the sweet gas zones in SGT-01, start oil production for well P1, TRB03 and TRB06. (I am assuming right here that all these wells are chosen because they are of close proximity to SGT-01 which allow them to have a better understanding of the oil profile in those wells). All these works aim to yield 200 barrels of oil per day by 3Q18 and monetise the sweet gas in SGT-01 before the year ends.

What does all these mean?

All these will mean that GSS will finally recognise their maiden revenue from their oil and gas venture. I shall attempt to do a brief calculation of how big this is for GSS.

For SGT-01,

8.49 BCF of gas is equivalent to 8617350 MMBTU of gas. As of current natural gas price, 1MMBTU cost USD$2.65 (but let’s discount it to USD$2.50)

Total gas revenue = USD$21,543,375 = SGD$ 28,006,387.50

Share of revenue for GSS = 31.4% of total gas revenue then 89% of PT SGT = SGD$7,826,664.45

Can’t assume the net profit as we are unsure of the cost required to produce the natural gas. But one noteworthy fact is that the gas found is sweet which is of high quality and can be sold for a higher price.

For oil,

Total oil revenue = 2.83 million barrels of oil x USD$50 per barrel = USD$141.5 million = SGD$183.95 million

Share of revenue for GSS = 23.5% of oil revenue and then 89% of PT SGT = SGD$ 38.5 million.

Net profit for oil (assuming cost of production per barrel is USD$15) = $SGD 26.9 million

For SGT-01 alone, total revenue (oil and natural gas) they can get out of this = SGD$46.3 million

For Well P1,

There are more than 3 potential pay zones according to their announcement.

For simplicity sake, let’s just assume that in Well P1 there is only 3 oil pay zone, and that the oil profile is similar to SGT-01. Meaning for that 3 pay zones, it yields 1.41 million barrels of oil (2.83 barrels divided by 2).

For simplicity sake, let’s just assume that in Well P1 there is only 3 oil pay zone, and that the oil profile is similar to SGT-01. Meaning for that 3 pay zones, it yields 1.41 million barrels of oil (2.83 barrels divided by 2).

Total oil revenue from P1 (assuming USD$ 50 per barrel) = USD$70.5 million = SGD$91.65 million

Share of revenue for GSS = 23.5% of total oil revenue and then 89% of PT SGT = SGD$18.76 million.

Net profit for GSS (assuming USD$15 per barrel COP) = SGD$13.41 million

For well TRB 03 and TRB 06,

Firstly we have to assume that TRB03 and TRB 06 are of close proximity to SGT-01 and they share rather similar oil profile. Because out of all the 24 abandoned oil wells that GSS could pick to work on, they have chosen these two, which I believe is after due consideration.

As we do not have much information on TRB03 and TRB06, we shall assume that both only had 2 oil pay zones. Total oil resources = 1.88 million barrels of oil

Total oil revenue from these 2 wells (assuming USD$50 per barrel) = USD$94 million = SGD$ 122 million

Share of oil revenue for GSS = 23.5% of total oil revenue and then 89% of PT SGT = SGD$25.5 million

Net profit for GSS (assuming USD$15 COP) = SGD$13.7 million

TOTAL GSS REVENUE FROM ALL THESE 4 WELLS = SGD$ 90.56 million

Assumptions Made,

- All wells have similar oil profiles as SGT-01, but to be conservative, I have assumed P1 only had 3 oil zones when there are more and also only assigning 2 oil zones each for TRB03 and TRB06 which should be much lesser than it could possibly be.

- I also assumed a lower oil price of USD$50 per barrel

- Cost of production is said to be USD$10 – $15 per barrel but I took the high end to calculate for all.

- Exchange rate used is USD/SGD = 1.3

What could go wrong?

Despite all the rosy picture about them striking oil, I would also like to analyse what can possibly go wrong. They may meet with some execution problem, where they are unable to successfully withdraw the oil or the gas.

SGT-01 is the very first exploration well that they drill. Supposedly, SGT-02 will be the next exploratory well and when they go there, the risk of not finding substantial amount of oil to commercialise will remain. The risk remains that when they drill in other areas of the Trembul operation area they might not find enough oil to commercialise it. So you can think of SGT-01 as the first battle won out of the many other battles that have yet to be fought.

Potential Catalysts

Their PE business have been doing rather well. The CEO have been talking about seeking to unlock value in the PE side of the business for sometime now. That could come in the form of a strategic divestment of partial ownership of the business or seeking a spin off of the PE side.

After all, the name GSS Energy is a clear indication that CEO Sydney wants to grow the oil business into a full fledge business to stand on its own. So I am looking forward to the oil business gaining some stability before CEO spins off the PE side of the business in 1-2 years time.

Of course, a clear catalyst for the oil business would be the discovery of more oil reserves in the area, which I think is very possible. If they continue with the strategy of digging exploratory wells near old abandoned wells, its very likely that oil can be found there.

In conclusion,

the total value of the 4 wells they are working on is worth SGD$90.56 million. At the price of $0.175 which is the price the CEO last bought from the open market, the market capitalisation is only SGD$ 86.8 million. Which is undervalued as they still have a functioning PE business delivering about SGD$75.61 million in revenue for FY 2016. Furthermore, this is only phase 1 of the oil business for GSS, they can still strike oil in other areas of Trembul with the 22 untapped abandoned old wells.

I would say that GSS is a long term play as the initial period of oil production is usually the hardest. Holding it for 2-3 years should see the real value being uncovered should everything goes according to plan.

PS I am vested.

Links where I took my information from:

http://infopub.sgx.com/FileOpen/SGX-GSSEL_20171213-Completion_of_well_SGT-01.ashx?App=Announcement&FileID=481906

https://www.nextinsight.net/story-archive-mainmenu-60/939-2017/11930-gss-energy-first-oil-discovery-with-sweet-gas-surprise